FHA Home Loans: Your Guide to Low Deposit Mortgage Choices

FHA Home Loans: Your Guide to Low Deposit Mortgage Choices

Blog Article

Exploring Home Loans: How Diverse Finance Programs Can Help You Achieve Your Imagine Homeownership

Navigating the landscape of home mortgage discloses a range of programs created to accommodate different economic situations, ultimately facilitating the journey to homeownership. From FHA loans that provide reduced down payment choices to VA financings that waive down repayment needs for eligible professionals, the choices can seem overwhelming yet encouraging. Additionally, conventional finances provide tailored options for those with one-of-a-kind credit scores accounts, while specialized programs sustain first-time buyers. As we check out these diverse finance alternatives, it becomes clear that understanding their ins and outs is essential for making knowledgeable decisions in your quest of a home.

Sorts Of Home Mortgage Programs

When thinking about financing options for acquiring a home, it is essential to understand the numerous kinds of home finance programs readily available. Each program is created to accommodate different customer scenarios, monetary circumstances, and building kinds, offering potential home owners with a variety of options.

Conventional loans, commonly used by personal lenders, are just one of the most usual choices. These car loans are not guaranteed or ensured by the federal government and may call for a higher credit history and a larger deposit. In contrast, government-backed finances, such as those from the Federal Housing Administration (FHA), Division of Veterans Affairs (VA), and the United State Division of Agriculture (USDA), offer even more adaptable certifications and reduced down repayment alternatives.

Adjustable-rate home loans (ARMs) offer rates of interest that can change over time, supplying reduced preliminary settlements but possibly increasing expenses later. Fixed-rate home loans, on the various other hand, maintain a constant rates of interest throughout the financing term, offering security in month-to-month payments. Comprehending these numerous car loan programs is critical for prospective house owners to make enlightened decisions that align with their monetary objectives and homeownership desires.

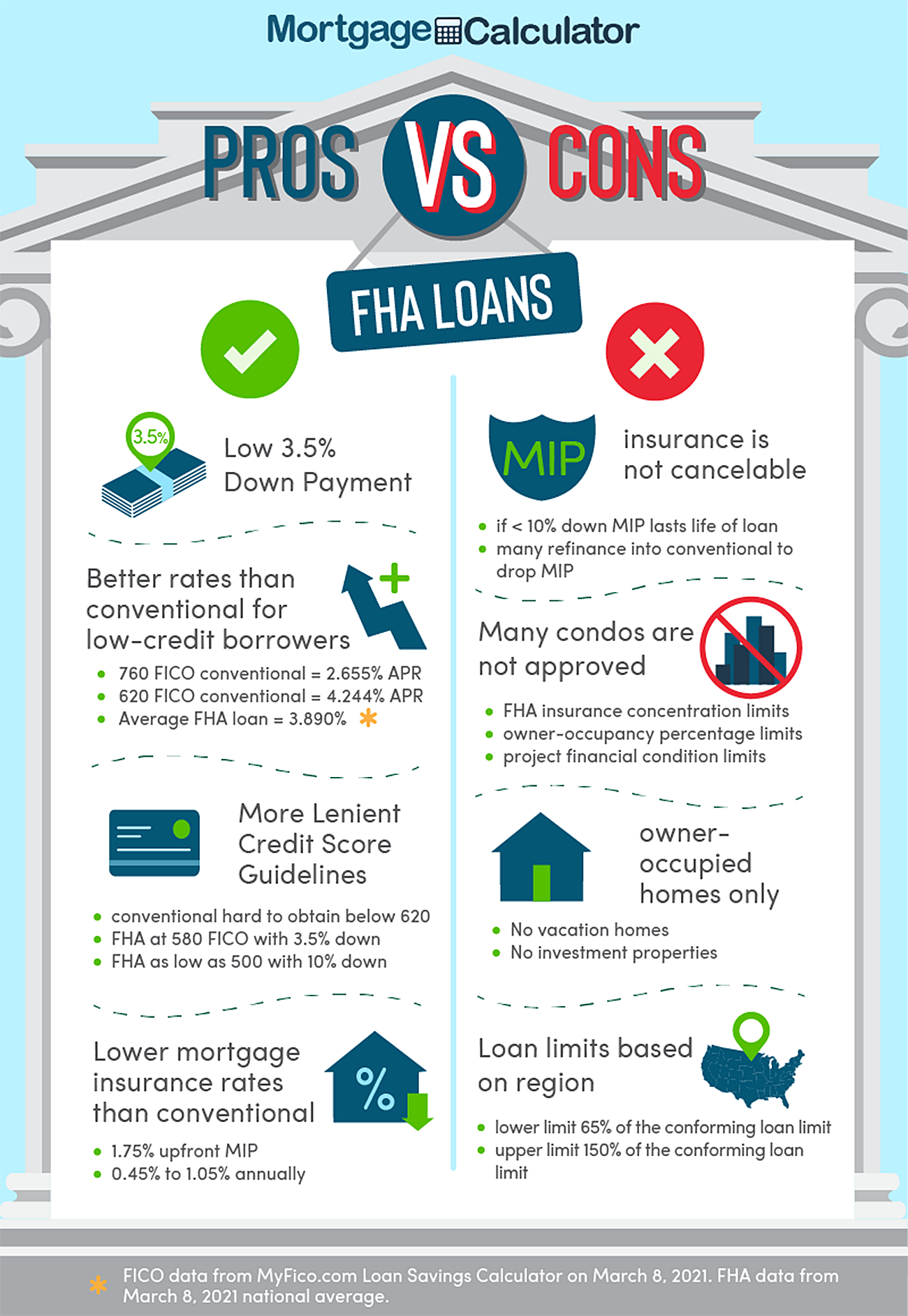

Advantages of FHA Financings

FHA loans offer numerous benefits that make them an eye-catching choice for lots of property buyers, particularly first-time buyers. One of the main benefits is the reduced deposit requirement, which can be as reduced as 3.5% of the acquisition cost. This substantially decreases the ahead of time financial concern for customers who may be struggling to conserve for a standard deposit.

Another benefit is the versatility in credit report needs. FHA financings permit lower credit report contrasted to conventional financings, allowing individuals with less-than-perfect credit report to receive financing (FHA home loans). Additionally, FHA financings are assumable, indicating that if you sell your home, the purchaser can take over your finance under the existing terms, which can be a selling factor in an open market

FHA financings additionally provide affordable rate of interest, which can result in lower month-to-month repayments gradually. These fundings are backed by the Federal Real estate Administration, providing a level of security for loan providers that might motivate them to supply much more desirable terms to borrowers.

Comprehending VA Loans

The special advantages of VA fundings make them an engaging choice for eligible professionals and active-duty solution participants seeking to acquire a home. Developed particularly to recognize army solution, these loans provide a number of crucial advantages that can dramatically reduce the home-buying process. Among the most significant benefits blog is the absence of a down repayment demand, which enables professionals to protect financing without the normal barriers that many novice homebuyers face.

Additionally, VA fundings do not require personal home mortgage insurance (PMI), additional lowering monthly payments and making homeownership much more budget-friendly. The rates of interest connected with VA finances are often lower than those of traditional financings, which can bring about significant savings over the life of the home loan.

Furthermore, VA car loans feature adaptable debt requirements, making them accessible to a broader array of candidates. The process is streamlined, frequently leading to quicker closings compared to traditional financing options. The VA's dedication to supporting professionals extends to ongoing assistance, making sure consumers can browse their homeownership journey with confidence. FHA home loans. Overall, VA lendings represent a beneficial source for those who have offered in the army, facilitating their desire for homeownership with desirable terms.

Traditional Car Loan Options

Adaptability is a trademark of conventional finance choices, which accommodate a large range of visit their website debtors in the home-buying process. These finances are not backed by any federal government agency, making them a popular selection for those looking for even more individualized lending options. Conventional finances generally can be found in two types: conforming and non-conforming. Adhering lendings stick to the guidelines established by Fannie Mae and Freddie Mac, that include car loan restrictions and borrower credit needs. On the other hand, non-conforming loans may go beyond these restrictions and are frequently looked for by high-net-worth people or those with unique financial circumstances.

Traditional car loans generally need a deposit varying from 3% to 20%, depending on the borrower and the loan provider's credit report profile. In addition, private home mortgage insurance policy (PMI) might be necessary for deposits below 20%, making sure that borrowers have several paths to homeownership.

Specialized Car Loan Programs

Several consumers discover that specialized financing programs can offer customized remedies to meet their special economic circumstances and homeownership goals. These programs are made to address particular requirements that standard lendings might not adequately satisfy. For example, new homebuyers can benefit from programs providing deposit aid or reduced mortgage insurance coverage premiums, making homeownership a lot more possible.

Veterans and active-duty army employees might discover VA loans, which offer affordable passion rates and the benefit of no down repayment. USDA finances cater to country buyers, supplying financing options with minimal down settlement demands for eligible residential or commercial properties.

Additionally, specialized car loan programs can support customers with lower credit report through FHA financings, which are backed by the Federal Real Estate Administration. These lendings usually include more adaptable qualification demands, allowing consumers Read Full Report to protect funding in spite of financial obstacles.

Conclusion

Finally, the diverse array of mortgage programs offered gives necessary support for people desiring attain homeownership. Programs such as FHA car loans, VA loans, and traditional alternatives cater to numerous financial circumstances and requirements. Specialized funding initiatives even more aid particular groups, consisting of new buyers and those with reduced credit rating ratings. Recognizing these options allows possible homeowners to navigate the complexities of funding, inevitably helping with notified choices and enhancing the possibility of effective homeownership.

From FHA lendings that provide lower down repayment choices to VA fundings that forgo down repayment demands for qualified professionals, the options can seem overwhelming yet promising. FHA car loans enable for lower credit score ratings compared to traditional fundings, making it possible for people with less-than-perfect credit scores to qualify for financing. In addition, FHA fundings are assumable, indicating that if you offer your home, the customer can take over your financing under the existing terms, which can be a selling point in a competitive market.

Adhering car loans adhere to the standards established by Fannie Mae and Freddie Mac, which include lending limits and consumer credit rating needs. Programs such as FHA financings, VA finances, and traditional choices cater to various economic circumstances and requirements.

Report this page